- AM/FM radio has 176 billion listening hours each year in the U.S.

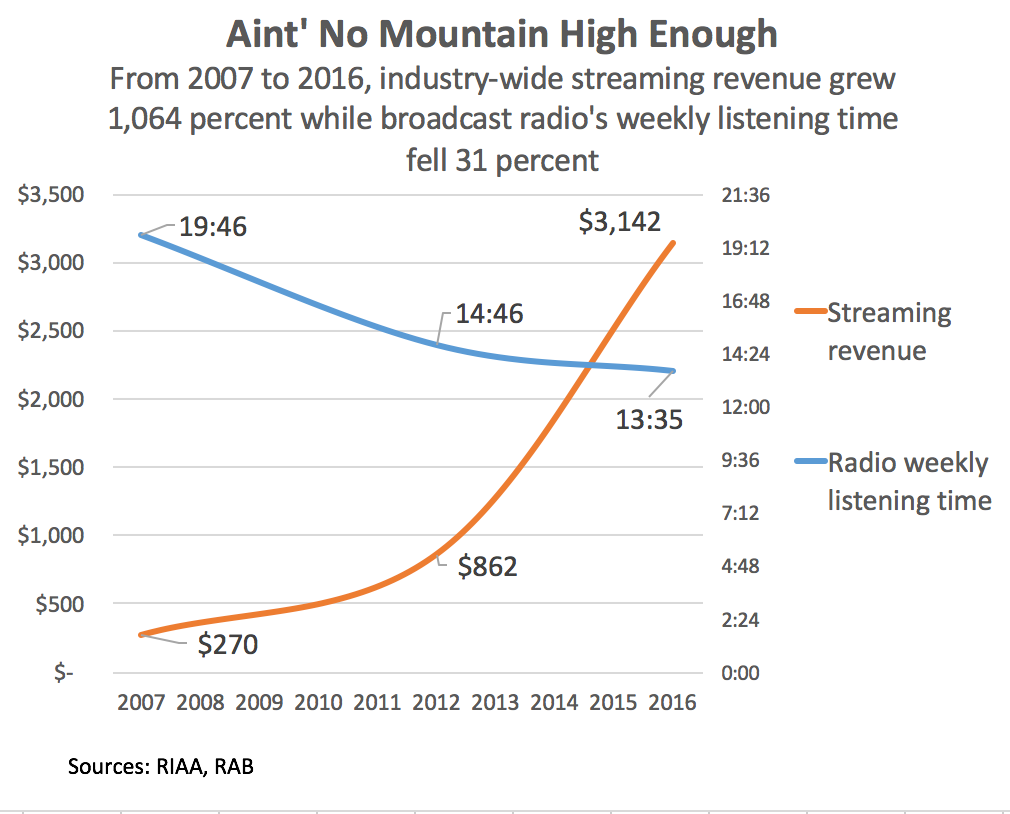

- The U.S. radio market is worth $15 to $17 billion annually.

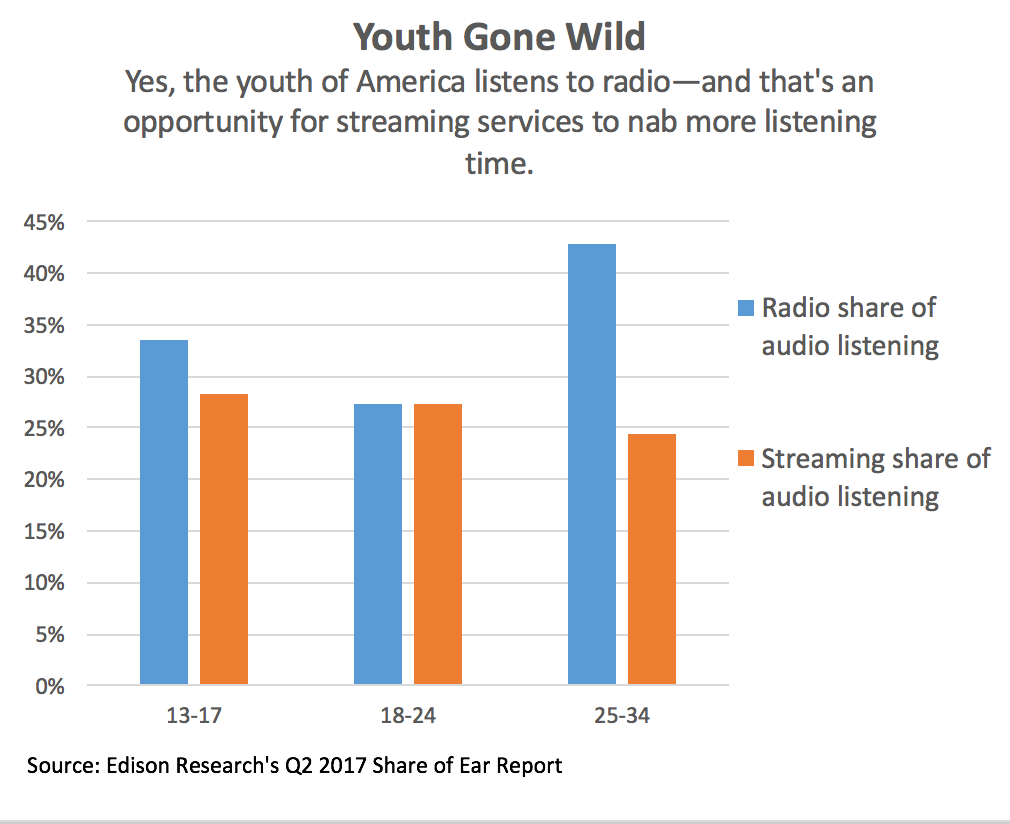

- The average American listens to 2 hours of AM/FM radio and just 36 minutes of streaming services each day.

- The youngest Americans are embracing streaming services, but they have hardly deserted AM/FM radio.