____________________________________

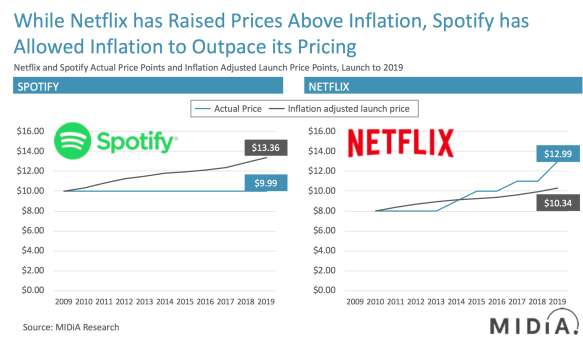

By Mark Mulligan of MIDiA and the Music Industry blogSongwriter royalties have always been a pain point for streaming, especially in the US where statutory rates determine much of how songwriters get paid. The current debate over Spotify, Amazon, Pandora and Google challenging the Copyright Royalty Board’s proposed 44% increase illustrates just how deeply feelings run. The fact that the challenge is being portrayed as ‘Spotify suing songwriters’ epitomises the clash of worldviews. The issue is so complex because both sides are right: songwriters need to be paid more, and streaming services need to increase margin. Spotify has only ever once turned a profit, while virtually all other streaming services are loss making. The debate will certainly continue long after this latest ruling, but there is a way to mollify both sides: price increases.