Beginning in 2006, the CRB stopped including a CPI based rate increase for mechanical royalties, but as inflation continues to grow (albeit slowly) will the Copyright Royalty Board continue to pretend songwriters aren’t impacted?

Guest post by Chris Castle of Music Technology Policy

It is difficult to understand the reasons why, but the current proposal for mechanical royalty rates before the Copyright Royalty Board do not include an index for inflation. Until a 2006 it was customary to include a rate increase for mechanical royalties, often indexed to the Consumer Price Index (not the best index to chose, but serviceable). This practice began in 1978 but has been denied to a generation of songwriters since 2006 when certain mechanical rates were frozen and capped. Why? Because them what had the power to make the rules made that new rule and abandoned the old rule. And in the face of the edict from the rulemakers, the ruletakers simply sucked it up. They got away with it for 70 years when they froze the rate at 2¢, so why not try it again?

But frozen is the new down. Even though we have enjoyed relatively low inflation in the years since 2006, the buying power of 9.1¢ in 2006 dollars has the buying power of approximately 7¢ in 2021 dollars. Conversely, in order to stand still and retain the buying power of 9.1¢ in 2021 dollars, the rate must increase to 12¢. Note that this inflation-adjustment is not an increase based on the inherent value of the song, it is simply standing still watching a game of thimblerig with the winning shell played off the table and out of sight.

Yet, the recommendation before the Copyright Royalty Judges brought by the major labels and publishers is that the 2006 rate be continued at 9.1¢ for another five years for all songwriters. (This rate is paid by record companies for physical and downloads, and they also want to freeze the rate for ringtones and “music bundles.”) To my knowledge, the streaming mechanical rate has not been indexed to inflation, at least not overtly as had been the case.

Unfortunately, songwriters have to hope that the self-appointed songwriter bargaining group before the Judges make the right bet on inflation–the one actual songwriter in the proceeding is bitterly opposed. There is no reason to believe they will because they haven’t for 15 years. And you know what they say about the definition of madness, shared or unshared.

Why am I concerned about inflation over the next five years (or more likely, stagflation when income declines and prices increase like right now)? Mostly because inflation is the most regressive tax of all and affects songwriter heirs, families and those relying on catalog royalties the worst.

Here’s a few indicators:

April Personal Income dropped 13.1%, which I believe is the largest decline in history. This is partly to do with the end of stimulus in March, but is still a remarkable number. Other benchmarks were also wobbly according to the Bureau of Economic Analysis:

Personal income decreased $3.21 trillion (13.1 percent) in April according to estimates released today by the Bureau of Economic Analysis (tables 3 and 5). Disposable personal income (DPI) decreased $3.22 trillion (14.6 percent) and personal consumption expenditures(PCE) increased $80.3 billion (0.5 percent).

Real DPI decreased 15.1 percent in April and Real PCE decreased 0.1 percent; goods decreased 1.3 percent and services increased 0.6 percent (tables 5 and 7). The PCE price index increased 0.6 percent. Excluding food and energy, the PCE price index increased 0.7 percent (table 9).

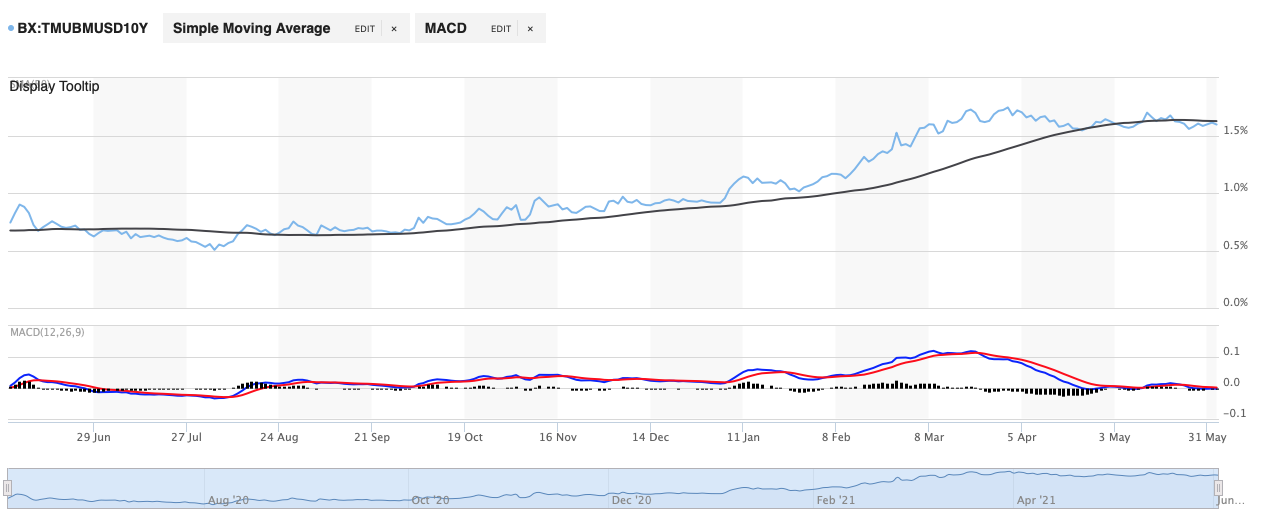

The interest rate on the 10 Year Treasury Note has increased over the last year to about 1.6% from about half that a year ago and is trending upward. Interest rates for the 10 year bond doubling in a few months is not a good sign and is highly unusual.

Perhaps more importantly, and admittedly a bit wonky, the 5 Year Breakeven Inflation Rate, a measurement of inflation expectations by the St. Louis Federal Reserve Bank, is now 2.60%.

Breakeven is a measurement of what market participants expect inflation to be in the next five or 10 years, on average, based on the spread between a nominal 10 year treasury and an inflation-linked bond of the same maturity (TIPS). (The cash flows from inflation-linked bonds are indexed by the non-seasonally adjusted consumer price index. If you want to get really wonky, it’s [(10-year nominal Treasury yield) – (10-year TIPS yield)]).

In plain English, this means that the super-experts in the bond market (vastly greater impact on daily life than the stock market) expect inflation to be 2.6% over the next five years. The trend line is up and to the right, which is bad for songwriters with frozen mechanicals.

So how can the correct answer from the smart people be to extend the freeze on mechanicals?

I’m all ears.