Guest Post by Mark Mulligan on Music Industry BlogReports suggest that Spotify may (finally) be about to launch video, as a means of differentiating in an increasingly competitive marketplace that is about to get a whole lot more competitive on the 9th of June (i.e. when Apple announces its long mooted arrival into the space). Spotify needs a differentiation point. It may be the runaway market leader but it doesn’t have the feature badge of identity that many of its competitors do (e.g. Rdio is the social discovery service. TIDAL is the high def service. Beats is the curation service etc.). However, even with a feature differentiation point, Spotify and all of its subscription peers face a more substantial challenge than competing with each other: they are collectively in danger of banging their heads on the ceiling of demand for music subscriptions.Behaviours Will Change, But SlowlyThe world is unequivocally moving from ownership to access and streaming will be a central component of this new consumption and distribution paradigm. 9.99 subscriptions however have no such mainstream inevitability. They are too expensive for most consumers but most crucially they require consumers to pay for music every month when most people instead spend when one of their favourite artists is in cycle with a new album, single or tour. Over time (a half generation or so) some consumers will have their behaviours modified, but the majority will not. In some sophisticated markets (such as South Korea, the Nordics and, to some degree, the Netherlands) subscriptions are showing some sign of edging towards a wider audience (though still far short of mainstream). In most major music markets though, they remain firmly locked in single digital percentage adoption ranges. They are niche services for the high spending aficionados.

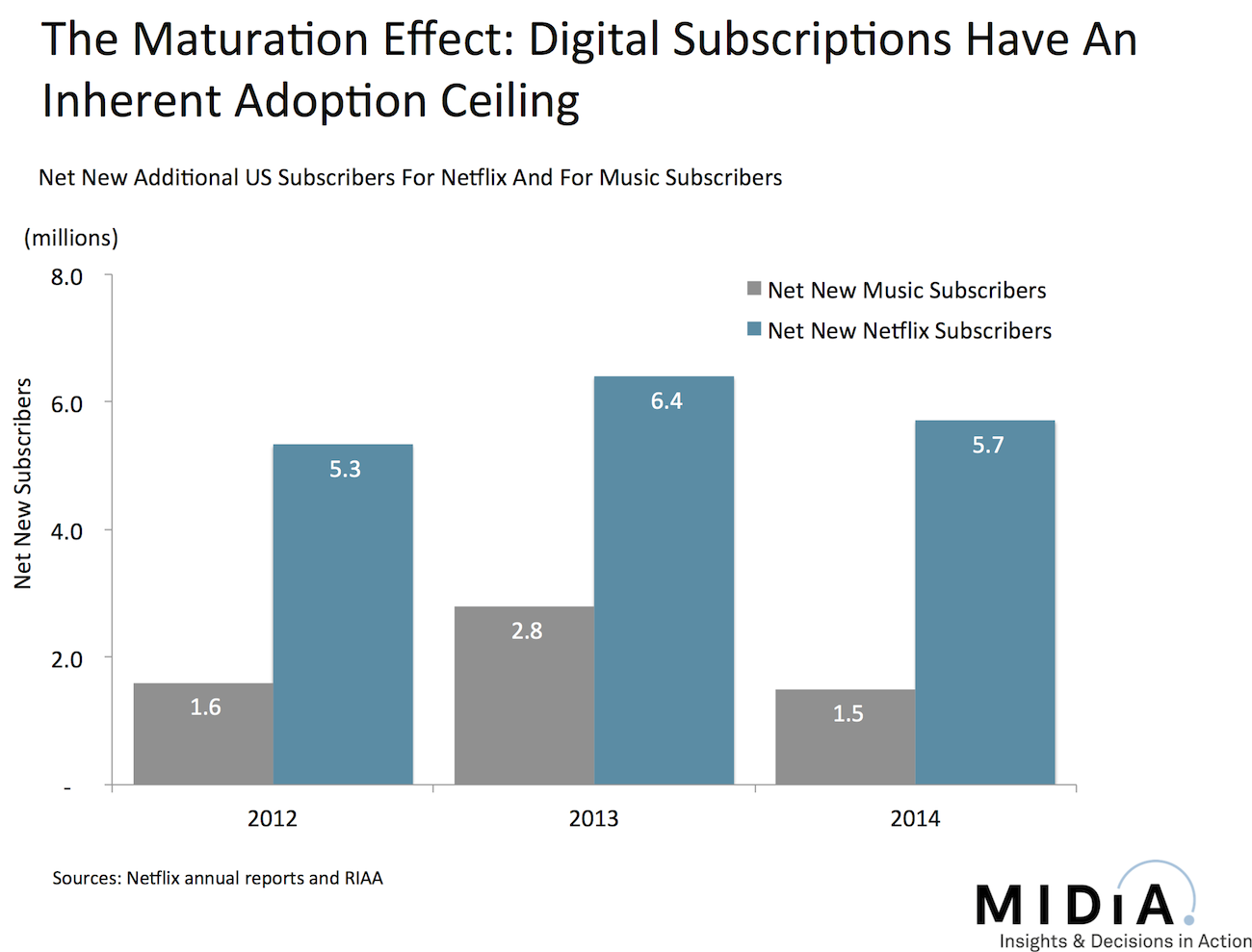

But this isn’t solely a music subscription problem. It is a dynamic of digital subscriptions more broadly. Take a look at the US. In 2014 net new subscribers (i.e. the amount of subscribers by which the market grew) fell to 1.5 million, down from 2.8 million in 2013 – which translated to a 46% decline in net adds. And that was in one of the highest profile years yet for subscriptions. Over the same time period, Netflix’s net new US subscriber growth fell from 6.4 million to 5.7 million, which was a more modest 11% decline in net adds.This is not to say either business model has run its course – far from it, and of course both sectors still gee in 2014 – but instead that premium subscriptions are not mass market value propositions. And once you have mopped up your early adopters and early followers growth inherently slows. The music industry may be locked in an identity crisis over how it deals with freemium services, but it needs to have a realistic understanding of just how far subscription services can go without lower price tiers and more ability for users to easily dip in and out and, ideally, pay as they go rather than being tied to monthly commitments.The incessant success of YouTube and Soundcloud show us that mainstream consumers want on-demand music experiences but the slow down of subscriber growth in the US shows us that the incumbent model only has a certain amount of potential. Sure, Apple will doubtlessly unlock a further tier of early followers to meaningfully grow the market, but it will only be a matter of time before it hits the same speed bumps.Access based models are the mainstream future, subscriptions can be too, premium subscriptions though are not.

But this isn’t solely a music subscription problem. It is a dynamic of digital subscriptions more broadly. Take a look at the US. In 2014 net new subscribers (i.e. the amount of subscribers by which the market grew) fell to 1.5 million, down from 2.8 million in 2013 – which translated to a 46% decline in net adds. And that was in one of the highest profile years yet for subscriptions. Over the same time period, Netflix’s net new US subscriber growth fell from 6.4 million to 5.7 million, which was a more modest 11% decline in net adds.This is not to say either business model has run its course – far from it, and of course both sectors still gee in 2014 – but instead that premium subscriptions are not mass market value propositions. And once you have mopped up your early adopters and early followers growth inherently slows. The music industry may be locked in an identity crisis over how it deals with freemium services, but it needs to have a realistic understanding of just how far subscription services can go without lower price tiers and more ability for users to easily dip in and out and, ideally, pay as they go rather than being tied to monthly commitments.The incessant success of YouTube and Soundcloud show us that mainstream consumers want on-demand music experiences but the slow down of subscriber growth in the US shows us that the incumbent model only has a certain amount of potential. Sure, Apple will doubtlessly unlock a further tier of early followers to meaningfully grow the market, but it will only be a matter of time before it hits the same speed bumps.Access based models are the mainstream future, subscriptions can be too, premium subscriptions though are not.Related articles