Music Technology UK’s new Sound Investments 2026: Back the Sector report makes a clear argument: the UK does not need to invent a music tech sector. It already has one. The problem is that it is not being backed at the scale needed to turn promising startups into global companies.

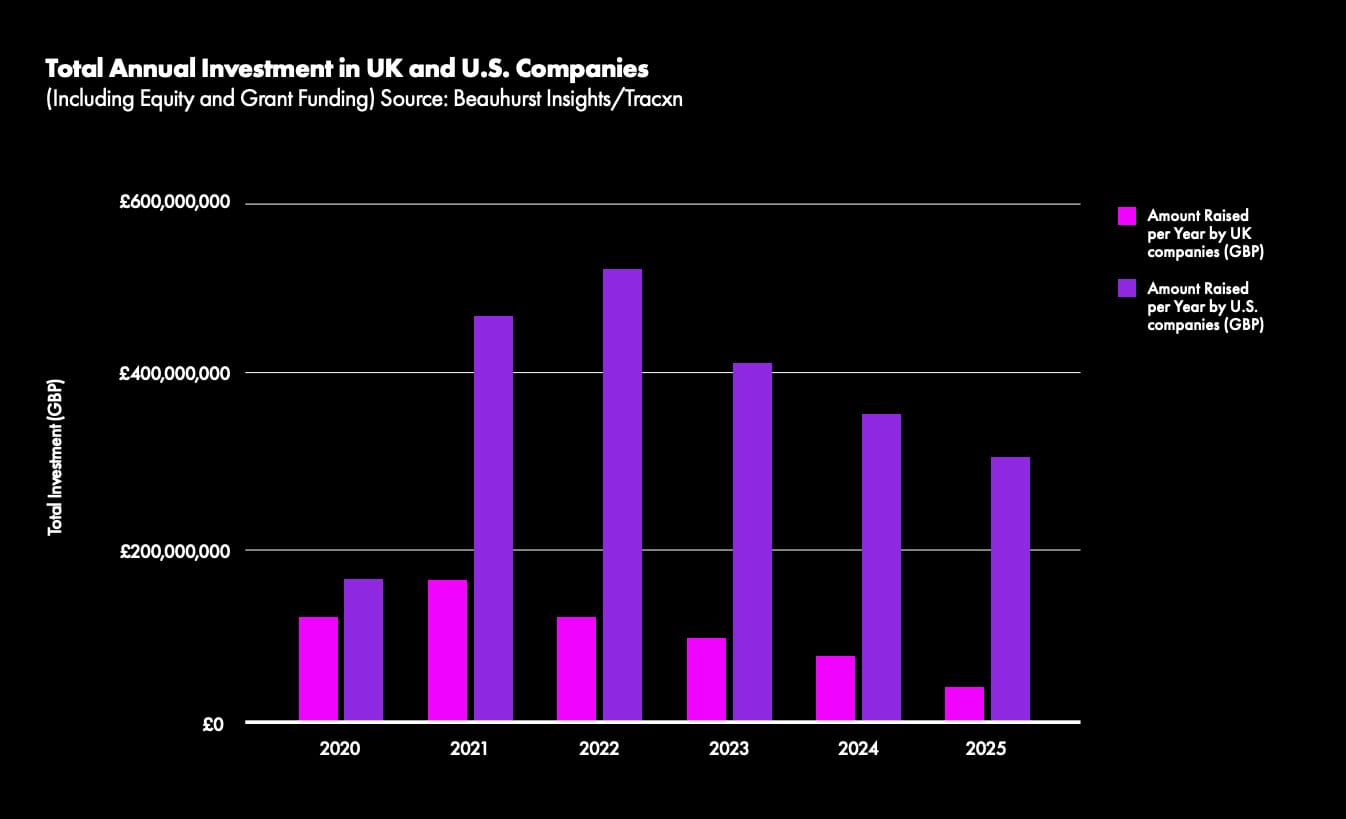

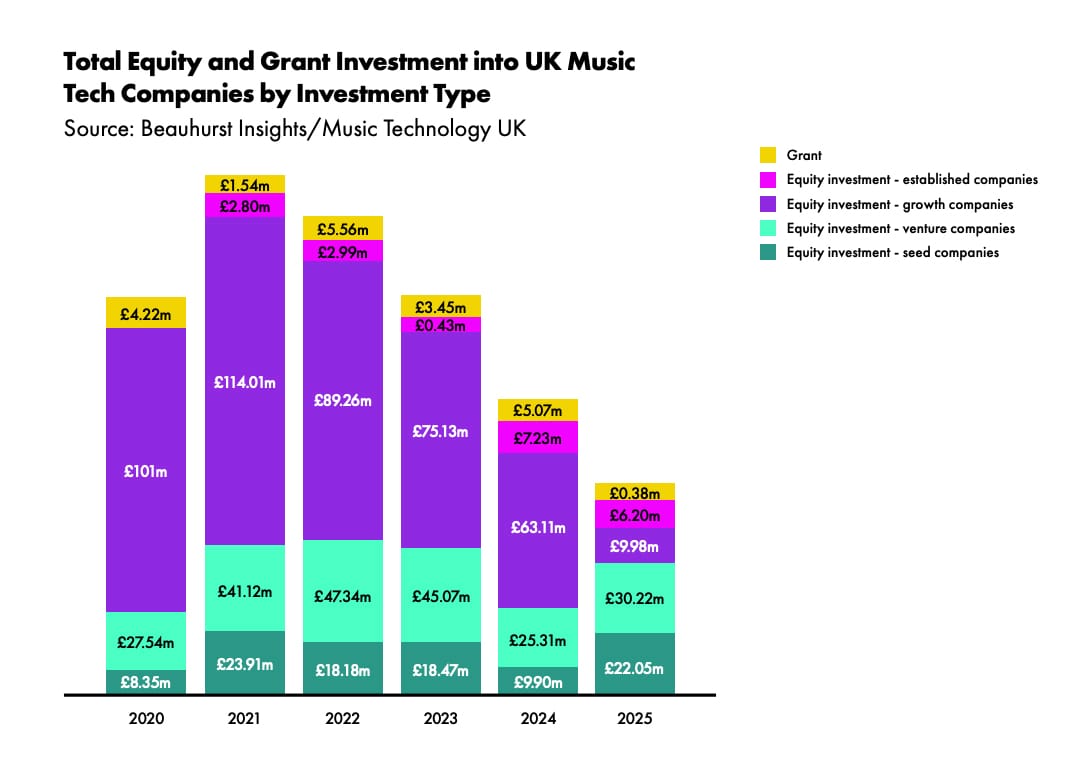

The report finds that UK music tech companies attracted more than £809 million in total investment between 2020 and 2025. But the trend line is worrying. Annual investment peaked at £183 million in 2021 before falling to £68.8 million in 2025, the lowest full-year figure in the period. That drop is far steeper than the broader UK tech market.

Here are the 7 biggest takeaways from this new report. Read and download the report in full here.

1. The UK's Music Tech Sector Has a Scaling Problem, Not a Startup Problem

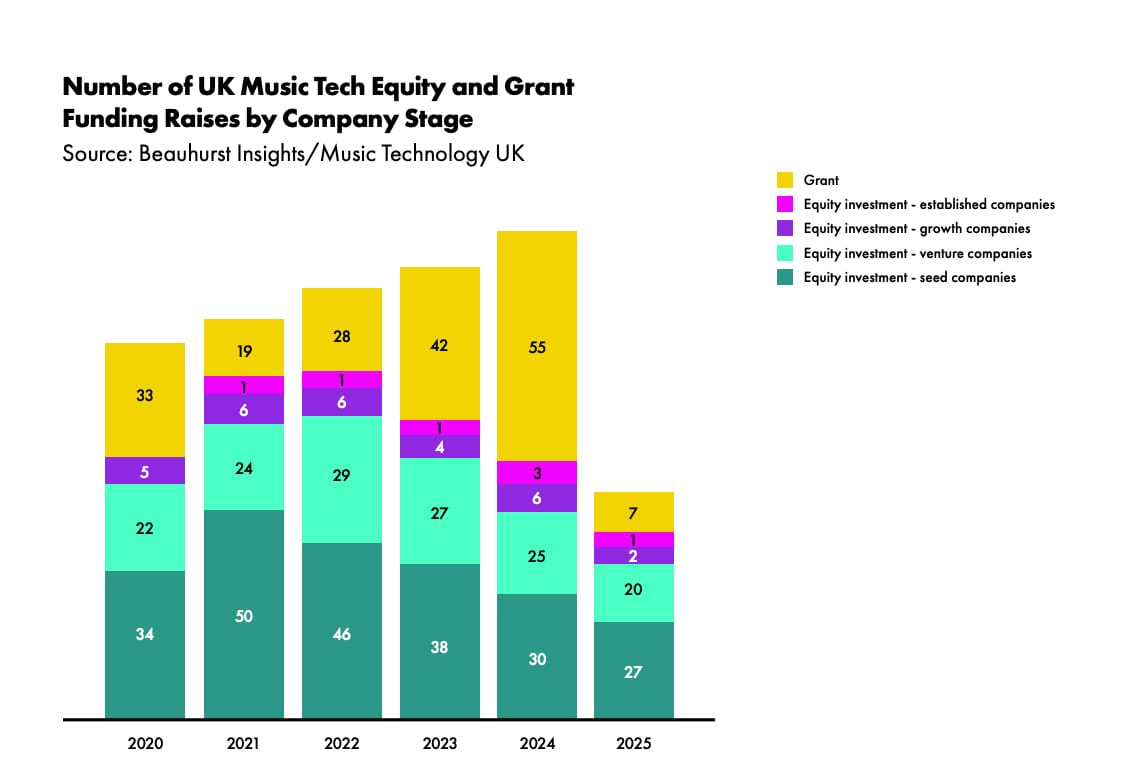

The report's most important finding is that the UK is still producing music tech startups, but it is struggling to help them grow into global companies. Seed-stage investment has remained relatively healthy and even increased in some areas. The real bottleneck appears after product-market fit, when companies need larger rounds to expand internationally, hire talent, and scale operations.

Growth-stage funding has collapsed from more than £100 million annually to just £10 million in 2025, creating what MTUK describes as a significant capital gap. In other words, the pipeline is working — but the bridge to the next level is missing.

2. AI Is Making Music Infrastructure More Valuable Than Ever

One of the report's strongest arguments is that AI may actually increase the value of many music tech companies rather than diminish it.

As generative AI expands, the industry needs better systems for ownership tracking, rights management, royalty accounting, attribution, licensing, and payment distribution. MTUK calls this the "middleware" layer of music — the infrastructure that sits beneath streaming services, labels, publishers, and creator platforms.

That means companies building royalty systems, rights databases, metadata tools, fingerprinting technology, and financial infrastructure may become some of the most strategically valuable businesses in the sector.

+Read more: "Exposing How the Live Music Industry Lies About Its Massive Carbon Footprint"

3. The Smart Money Is Already Betting on Rights and Royalties

If there's one category investors seem consistently interested in, it's music rights infrastructure.

The report found that Data, Analysis, Royalty, and Finance Solutions companies attracted the highest levels of investment activity and acquisition interest between 2020 and 2025. These businesses are often easier for investors to understand because they resemble SaaS, fintech, or enterprise software companies rather than traditional music businesses.

That's encouraging because these tools also happen to address some of the industry's most persistent problems: transparency, attribution, and getting artists paid accurately.

4. America Keeps Buying What Britain Builds

Perhaps the most uncomfortable finding in the report is that U.S. investors appear more interested in acquiring UK music tech companies than funding them through their growth stage.

American firms accounted for a significant share of acquisitions while representing a much smaller portion of investment rounds. The implication is clear: the value of UK music tech is being recognized, but often only once companies are mature enough to be purchased.

The danger is that Britain develops the intellectual property, talent, and innovation, while the long-term economic value migrates elsewhere.

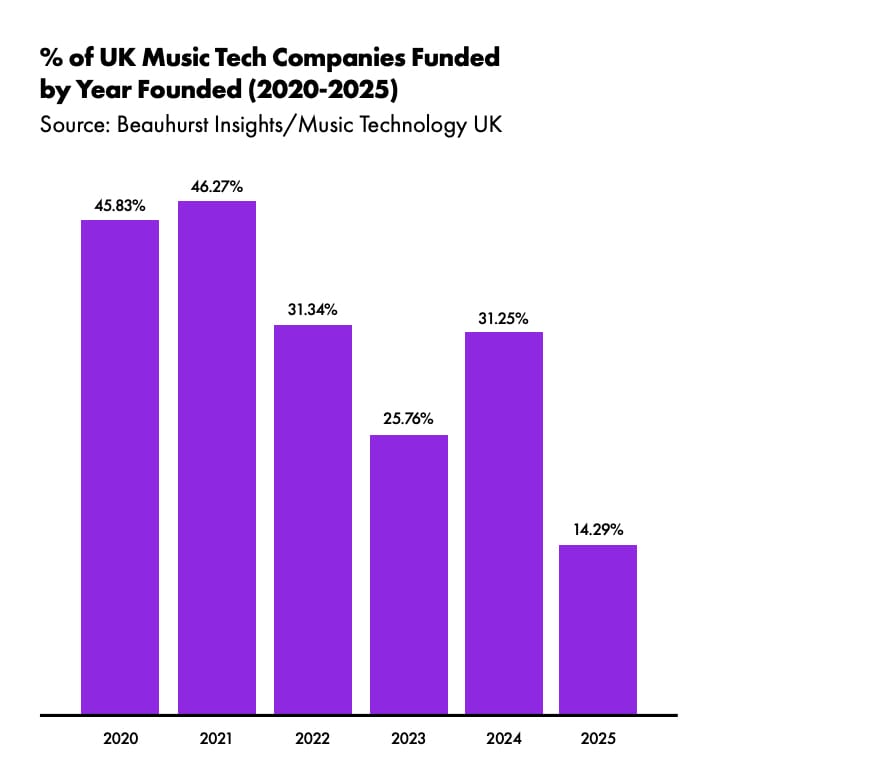

5. Grant Funding Is Drying Up

Another concern is the sharp decline in grants. Grant funding reached a six-year low in 2025, and the average grant size has fallen dramatically over the last several years. For many music tech startups, grants represent the first external validation they receive before attracting private investors.

Without that early support, fewer founders may be able to survive long enough to prove their ideas.

+Read more: "What Vinyl Boom? Gen Z Is Driving a Surge in CDs"

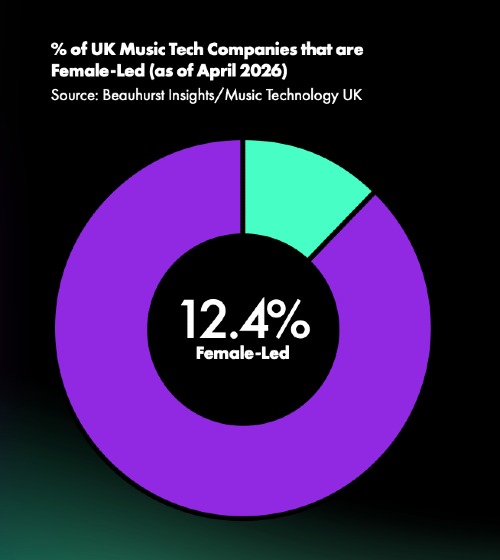

6. Diversity Progress Remains Slow

The report also raises concerns about representation. Only 12.4% of UK music tech companies are female-led. While that is somewhat better than parts of the broader tech ecosystem, it remains significantly below where many industry observers would like to see the sector.

If music tech is helping shape the future infrastructure of music, the report suggests it should better reflect the diversity of the creators and audiences it ultimately serves.

7. Music Tech Is Still Invisible in Government Policy

One of MTUK's biggest frustrations is that music tech remains largely unnamed in major creative-industry initiatives. The report points out that government policy frequently references music, gaming, film, and television, but rarely acknowledges the technology companies that power those sectors.

Gaming, for example, benefits from dedicated tax incentives, funds, and policy frameworks that make it easier for investors to understand and support. MTUK argues that music tech deserves similar recognition if the UK wants to remain competitive.

The report's core message is simple: music tech is no longer a niche sector. It has become essential infrastructure for the modern music business. The opportunity is enormous — but only if the companies building that infrastructure can survive long enough to reach their full potential.